Hemp

Lack of fiber processing infrastructure holds back hemp industry

Despite its potential, the growth of the embryonic hemp fiber industry in North America is being constrained by the lack of processing infrastructure, reveals a New Frontier Data article.

While hemp fiber was once a common crop across the continent, the 81-year ban caused all facilities capable of processing it to close and hemp was eventually replaced by other materials. Therefore, almost the entire fiber supply chain needs to be rebuilt from scratch.

The article published by New Frontier Data addresses gaps in the industrial hemp supply chain in North America, predominantly in primary processing, which essentially consists of decortication, with a special focus on the United States of America. Decortication is a mechanical process that separates hemp stalks into fiber and hurds ou shivs (loanwords used by the industry to identify the woody core of the plant).

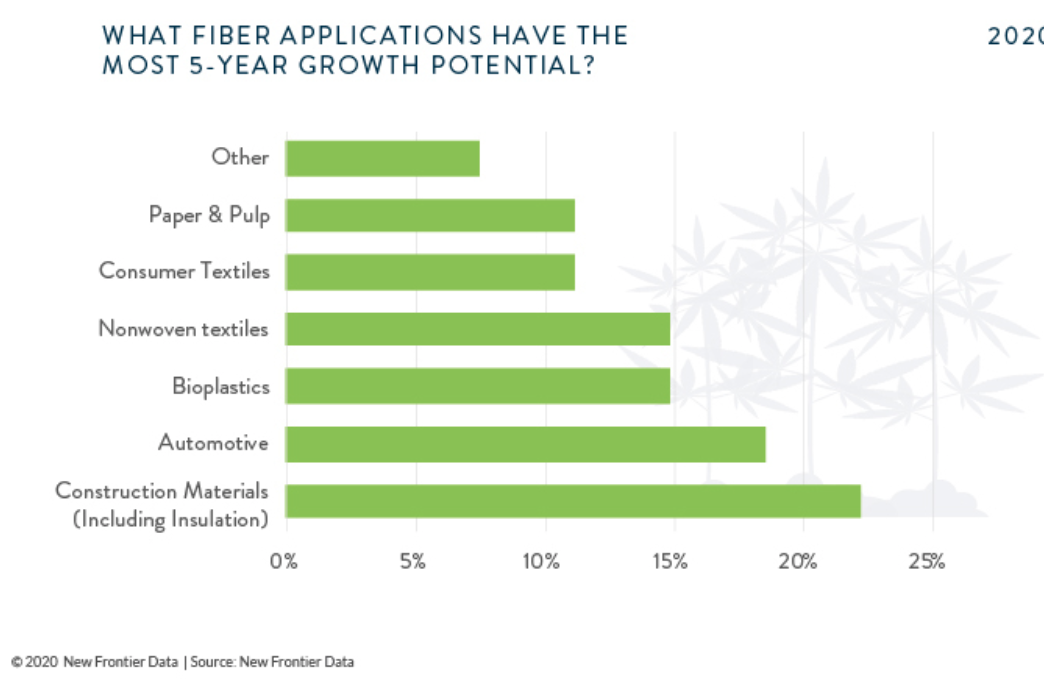

5-year potential of industrial hemp fiber applications, according to New Frontier Data

This is the most essential process in the entire production chain, as it creates a stable supply source of fiber and shivs, which can then move on to further processing for end use in manufacturing products.

North America (like Portugal, for example) has a shortage of processing capacity, manifested by the lack of facilities capable of stripping hemp fiber. The shortage is largely attributed to the “tail-in-the-mouth fish” that it makes no sense to build a processing facility when there is little hemp to be grown. On the other hand, it also makes no sense to grow hemp on a large scale without a factory with the capacity and scale to process it. The CBD production industry was largely responsible for the explosive increases in industrial hemp acreage, but this is no longer the case. Right now, more hemp is being grown than can be processed through existing infrastructure. This phenomenon creates several situations in which the market is faced with disruptions in terms of processing and in terms of the supply of transformed material.

Instability discourages farmers and investors

Extreme volatility in fiber prices discourages farmers and processors from making large investment commitments, while erratic and uneven supply complicates manufacturing and processing efforts. Fiber processing facilities can also be extremely capital intensive – the cost of construction can range from US$3 million to US$25 million – and, because of the economic infeasibility of transporting raw hemp stalks, processing facilities are geographically limited to the processing of hemp grown within a radius of not more than 150 kilometres.

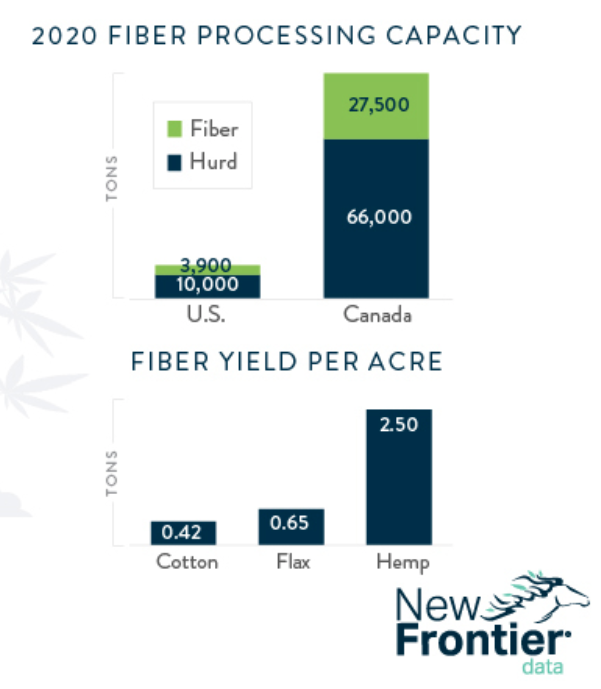

US and Canadian Processing Capacity and Fiber Yield per Acre, according to New Frontier Data

In addition, fiber processing offers lower margins when compared to CBD processing. Early entrants into the industrial hemp-derived CBD industry faced a number of barriers when it came to consumer education, government regulation and logistics, but they reaped enormous gains before the market became saturated. Early entrants into fiber will face similar challenges, without the equivalent promise of such quick and significant profits.

Despite the challenges, some companies invest

As of December 2019, the processor Panda Biotech, based in Dallas, has announced plans to build, by 2021, the largest hemp processing facility in North America – capable of processing more than 130.000 tons of hemp fiber annually. also the Collective Growth Corporation – a special purpose acquisition company (SPAC) formed by founder and former Canopy Growth CEO Bruce Linton – announced in May its intention to invest $150 million in the hemp fiber industry in 2021.

Numerous smaller-scale operations, respectively, have invested finance capital around hemp hotspots in Texas, Montana, and South Dakota, among others. Due to the large capital investment required, the nature of this commodity based on the volume of processing and also due to geographic limitations to the raw material supply, there is a significant advantage for the early adopters of primary fiber processing. This market dynamics – which results particularly from geographic limitations – means that the early presence of primary processors in a given area is likely to attract secondary processors, concentrating hemp fiber production close to regional centres. These regions will be the first to obtain returns in scale and thus enjoy competitive advantages in attracting investments and opening new markets.

The result will be that, given the considerable barriers to entry and its importance to the fiber supply chain in general, primary processing continues to be the main driver of production chain disruptions, which significantly delay the growth of the industry. .

_____________________________________________________________________

Featured Image: Rights Reserved – Hemp Inc.

____________________________________________________________________________________________________

[Disclaimer: Please note that this text was originally written in Portuguese and is translated into English and other languages using an automatic translator. Some words may differ from the original and typos or errors may occur in other languages.]____________________________________________________________________________________________________

![]()

What do you do with €3 a month? Become one of our Patrons! If you believe that independent cannabis journalism is necessary, subscribe to one of the levels of our Patreon account and you will have access to unique gifts and exclusive content. If there are many of us, we can make a difference with little!

ICBC Berlin shines again. It's the beginning of a new era for the cannabis industry in Germany

ICBC Berlin was the first major international cannabis conference to take place after the legalization of adult use in...

USA: Mike Tyson products recalled for mold contamination

California authorities have issued a mandatory recall notice for two products from Mike Tyson's cannabis brand,...

4:20 is coming and there are celebrations in Porto and Lisbon

The date for celebrating cannabis culture is approaching! This Saturday, April 20th, is the day when...

Paul Bergholts, alleged leader of Juicy Fields, detained in the Dominican Republic

Paul Bergholts, the alleged leader of the Juicy Fields pyramid scheme, has been detained in the Dominican Republic and will be subjected to...

Cannabinoids reveal promising results in the treatment of Borderline Personality Disorder

An investigation carried out by Khiron LifeSciences and coordinated by Guillermo Moreno Sanz suggests that medicines based on...

Juicy Fields case: 9 detained by Europol and Eurojustice. Scam exceeds 645 million euros

A joint investigation conducted by several European authorities, supported by Europol and Eurojust, culminated in the arrest of nine suspects...

Regular cannabis users may require more anesthesia during medical procedures

Regular cannabis users may require more anesthesia during medical procedures to remain sedated compared to...

The future of CBD in Japan: How legal reforms will shape the market

Late last year, Japan took a big step towards cannabis reform after approving...

Portugal: GreenBe Pharma obtains EuGMP certification at Elvas facilities

GreenBe Pharma, a medical cannabis company located in Elvas, Portugal, has obtained EU-GMP certification under...

Álvaro Covões, from Everything is New, buys Clever Leaves facilities in Alentejo for 1.4 million euros

Álvaro Covões, founder and CEO of the show promotion agency 'Everything is New', which organizes one of the biggest festivals in...